June 2026 Commentary

GLOBAL MARKETS

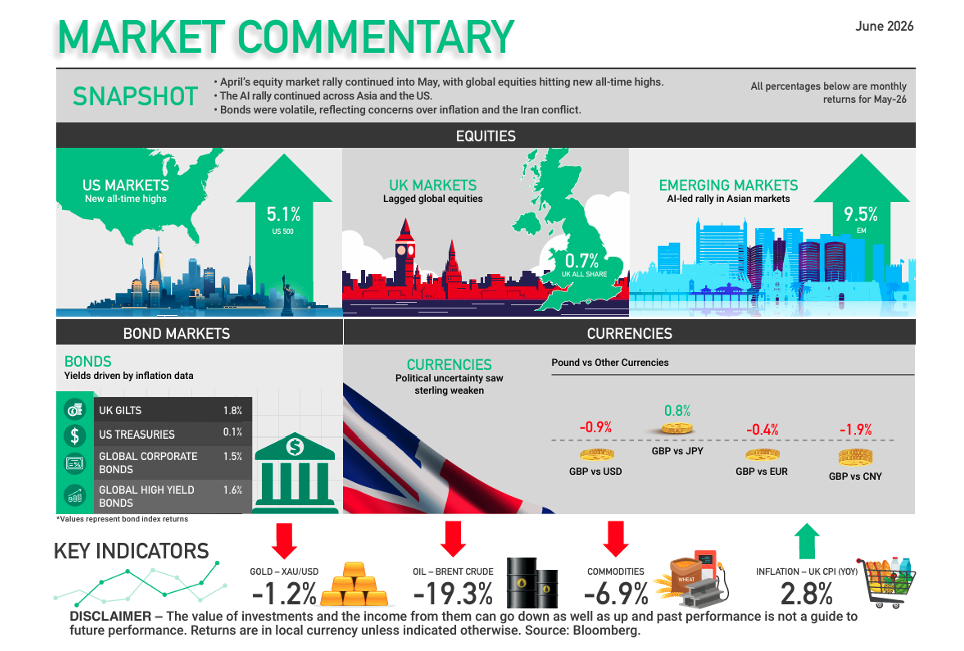

Market optimism over AI trumped inflation concerns around the continued closure of the Strait of Hormuz. Growth, led by a surge in semiconductor stocks, outperformed Value, and Asia-Pacific was particularly strong.

US MARKETS

Hit new highs on strong earnings

US indices notched fresh records as economic data and a strong earnings season overshadowed geopolitical risks and inflation concerns. Inflation hit 3.8%, and PPI was even higher, but markets shrugged this off, as well as a downgrade in Q1 26 GDP. Technology led the way, particularly semiconductors. The S&P 500 rose and NASDAQ managed 8.4%. Some of the individual stock moves were extraordinary – Micron Technology surged 88% and became a trillion-dollar market cap company. SpaceX laid the groundwork for the largest IPO in history, raising US$40-80bn and an implied valuation potentially close to US$2tn.

Up 5.1% (US 500)

UK MARKETS

Moved ahead but lagged peers

UK equities underperformed peers but still delivered positive returns. The structural bias towards energy and defensive sectors continued to detract in a market environment favouring growth and technology, so very much a continuation of what we saw in April. The big AI trade seemed to pass the UK by. BP was particularly weak on the back of further boardroom instability. Political uncertainty was unhelpful as the market priced in a more left-wing narrative going forward.

Up 0.7% (UK All Share)

EUROPEAN MARKETS

Positive overall on some technology exposure

European equity markets were positive overall, with the STOXX 600 up, but it lagged the strength that we saw in the US and in Asia. It has some technology exposure, but nothing like the scale and size that is evident in the US. As with the UK, it was energy, financials and defensives that lagged. Economic data continued to come in noticeably below expectations, in a continuation of the trends that were seen the previous month. Eurozone GDP expanded by a mere 0.1% in the first quarter.

Up 3.2% (Euro 600 Index ex UK)

JAPAN MARKETS

Powered ahead on market optimism

TOPIX briefly eclipsed the previous February high, but the Nikkei was far stronger, at one point passing the 65,000 mark. Optimism over an end of the Iran conflict (Japan has a major energy supply deficit), the strength of local Asian markets such as South Korea, gains for technology stocks, and domestic political optimism all combined to drive equity markets higher. The Bank of Japan intervened heavily to support the yen. Domestic demand remained resilient despite the inflationary impact of higher raw material costs.

Up 6.2% (Japan Index)

Key Points:

• Global equities shrugged off concerns over inflation and hit new highs on a buoyant earnings season and further AI-led optimism.

• Optimism over an end to the Iran conflict saw oil fall, and gold fell on reduced concerns over rate rises – clearly an unhelpful backdrop for energy and precious metals sectors.

• Both South Korea and Taiwan were buoyed by the rally in semiconductor stocks. South Korea is a particularly concentrated market, with Samsung and SK Hynix accounting for over half the market. Both stocks rose dramatically in May.

• Geographically, it was Pacific ex-Japan that led the charge, with the UK the noticeable laggard. Thematically, it was growth over value.

Key Points

• The US dollar index rose mid-month, reflecting expectations of a more hawkish US Fed in the wake of rising inflationary pressures, and worse than expected CPI and PPI numbers.

• Despite intervention by the Bank of Japan, which began at the end of April, the yen remained weak against a robust US dollar.

• Sterling fell from U$1.359 to finish the month at U$1.343, reflective of US dollar strength.

• The euro touched one-month lows as the Eurozone growth outlook dimmed, though it stabilised as markets fully priced in at least two ECB hikes.

Key Points

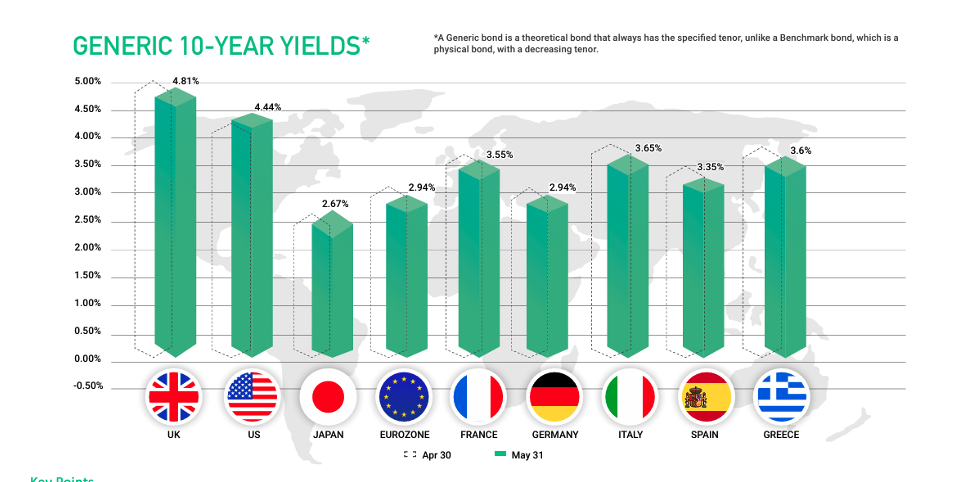

• US 10-year Treasury yields climbed above 4.65% mid-month on inflation and interest rate concerns. Optimism on an end to the Iran conflict, alongside the falling oil price, allowed yields to ease back.

• Gilts were volatile. The 10-year yield hit 5.18% mid-month, before retreating sharply on Iran, the falling oil price and perceptions of better-than-expected inflation figures.

• At the shorter end of the curve, US 1-year yields actually rose, as interest rate expectations were repriced, but across Europe they fell, most noticeably in the UK.

• UK gilts and sterling corporate debt had some of the best returns over the month, but it came with elevated volatility. The buoyant equity markets were helpful, sentiment-wise, for global corporate and global high yield markets.